Advanced CVA Methodology

Summary

This document describes how B3 ADV CVA capital charge is calculated in response to the new regulatory capital charges designed to capture the risk associated with the Credit Value Adjustments introduced by Basel III.

Introduction

Basel III introduced a new Regulatory Capital Charge associated with Credit Value Adjustments. CVAs are adjustments made to the value of OTC derivatives to incorporate Couterparty Credit Risk. Changes in CVA exposures could produce significant gains or losses. Basel III requires financial institutions to hold capital against this risk. This charge is a one-side adjustment that takes counterparty risk into account but does not reflect the risk of the bank to the counterparty.

Calculation Approaches

The Basel committee provides two methods to calculate CVA: Standardised and Advanced.

CVA rules prescribe that banks with a VaR model waiver for Market Risk and IMM models for Counterparty Credit Risk must use the Advanced CVA method unless the relevant regulator decides that for certain portfolios the bank can use the standardised version.

Rules and reporting Requirements

The CVA rules have taken effect on the 1st of January 2013.

The capital calculation is based on the application of the bank’s market risk VaR model to the relevant counterparty exposures and hedges. The table below shows the differences between the Market Risk VaR and the new Advanced CVA VaR model.

| Aspects | ACVA | Market Risk |

| Calibration | 99%, 10day VaR and stressed VaR | 99%, 10 day VaR and stressed VaR |

| Capital Multiplier | Same as Market Risk | Entity Specific |

| Averaging | Max of most recent and multiplier times three months average | Max of most recent and multiplier times 60day average |

| Calculation Frequency | Min of monthly, though daily capability required | Daily |

The ACVA capital charge is therefore

ACVA=Max(Spot CVA VaR, Multiplier * Average CVA VaR)+Max(Spot CVA VaR, Multiplier*Average CVA Stressed VaR)

ACVA Reporting

The ACVA capital charge is based on monthly calculations and more frequent capability for both regulatory and internal management information

Exposures

Unlike the accountaing CVA used by the Front Office which only applies to a subset of exposures (on the basis of their inclusion in the derivatives pricing), the Regulatory CVA capital charge applies to all derivatives arising from OTC derivatives, including the CCPs.

The CVA Regulatory Capital charge is required to be held even if the exposures do not feed the accounting CVA irrespective of whether they are booked in the trading or banking books.

Even though the ACVA charge requires a firm to have a counterparty risk IMM permission, the rules acknowledge tht certain smaller portfolios may use the CEM (Current Exposure Method) instead. In such cases, the CEM exposure are included in the ACVA charge alongside the IMM exposures.

PRA has introduced a materiality threshold for CEM exposures. Should the CEM amount be above the threshold, they will be included in the Standardised CVA charge rather than the Advanced CVA charge.

Exposures from SFTs (Repos) will not be subject to the CVA charge unless the regulator decides that they give rise to material CVA loss exposures. PRA has subsequently confirmed plans to introduce threshold for SFTs above which the exposures woud be subject to CVA charge. Should Repos be included in the CVA charge calculations, they will be calculated under the Standardised CVA since they constitute a material non-IMM portfolio. CCP exposures were included in the CVA capital charge until the CCP rules were finalised. Client legs of cleared OTCs and ETFs should also be included until the CCP rules were finalised.

| Products | PRA |

| OTC derivatives: IMM | Included in ACVA |

| OTC derivatives: CEM | If <threshold, include in ACVA

If >threshold, include in SCVA |

| OTC derivatives: CCP | Exclude from CVA |

| SFTs | If <threshold, include in ACVA

If >threshold, include in SCVA |

| Client legs of cleared OTC and ETF derivatives | Include in CVA |

Hedges

The Regulatory rules define the list of the hedges that are eligible to be included in the ACVA capital charge. These hedges are:

- Single name CDS

- Single name contingent CDS

- Financial Guarantees

- Other equivalent hedging instruments that reference the counterparty directly

- Index CDS

- CD Swaptions (Single name and index)

To be eligiblr for ACVA capital charge, hedges must be held for the purpose of mitigating CVA risk and managed as such. This means that otherwise eligible instruments that are held elsewhere in the bank (such as CDS held for marketing purposes) should not be included in the ACVA capital charge.

Inputs to ACVA capital calculation

Inputs are:

- Exposures (IMM, CEM, SFTs) and EE Profiles

- Hedges (CS01)

- Market data (Cs, LGD, IR)

Key exposure and hedge input data attributes to support methodology are as follows:

| Data Attribute | Exposures | Hedges |

| Value | Eff Exposure profile for CS01 tenor generation | CS01 per Tenor |

| Counterparty | Lowest counterparty level | Lowest counterparty level |

| Ultimate Parent | Parent Name | Parent Name |

| Market data Curve | Counterparty curve | Counterparty curve |

| CVA sector | Corp/Finance/Energy | Corp/Finance/Energy |

| Currency | Country of counterparty | Country of counterparty |

| Credit Rating | Rating of counterparty | Rating of counterparty |

Exposures

The Basel III ACVA rules require banks to use specified regulatory formulae to generate the inputs to their CVA VaR models. These formulae use exposure and market data to derive CS01. The inputs are derived in a two steps process.

- Convert Exposure inputs into a standard format

- Combine Exposure and Market data using regulatory formulae.

There are four different sources of exposure. In three of these cases, the exposures need to be converted into EE (Expected Exposure) and stressed EE values by tenor.

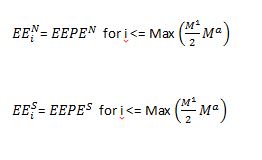

IMM EEs for the collateralised trades not using the Shortcut Method will be represented by tenor. No further calculation will be required.

IMM EEs calculated under the shortcut method is determined using normal and stressed market data. Constant EE profiles are constructed by setting EE to be the same of the EEPE (Effective Expected Positive Exposure) for all ternor points out to the maximum of (i) half the longest maturity in the netting set and (ii) the notional weighted average maturity in the netting set.

Where:

is the Expected Exposure calculated under normal data for tenor i

is the Expected Exposure calculated under normal data for tenor i

is the Expected Exposure calculated under stressed conditions for tenor i

is the Expected Exposure calculated under stressed conditions for tenor i

![]() Effective Expected Positive Exposures calculated under normal and stressed conditions

Effective Expected Positive Exposures calculated under normal and stressed conditions

is the notional-weighted average maturity of the netting set

is the notional-weighted average maturity of the netting set

is the longest maturity in the netting set

is the longest maturity in the netting set

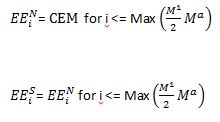

CEM Trades

For the CEM (Current Exposure Method) trades, a constant EE profile is used by setting the EE equal to the CEM for all tenor points out to the maximum of half of the longest maturity in the netting set and notional-weighted average maturity in the netting set. Stressed version of CEM don’t normally exist, therefore the input to the stressed CVA VaR charge should be the same as the input to the normal CVA VAR charge for these trades.

SFTs

SFTs are included in the CVA calculation if they breach a given materiality threshold. Being non-IMM portfolios, if they exceed the materiality threshold they will be processed by the SCVA charge.

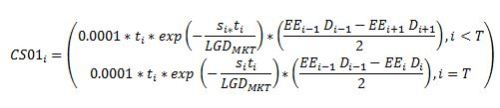

For SFTs, a separate EE is produced by tenor for ech netting set. Some counterparties will have multiple netting sets and EE profiles since they use multiple IMM models or a combination of full IMM, shortcut and CEM methods.

The EE profiles for each counteraprty need to be aggregated (preserving the term structure) prior to the application of the regulatory formuale that converts EEs into CS01. This is because the the regulatory formulae place most of the resulting risk in the final tenor bucket. This means that an EE profile that ends at year 5 tenor and an EE profile that ends at 20 year tenor will produce 2 different CS01 profiles if they are correctly aggregated prior to the application of the formulae rather than incorrectly having fomulae applied and then aggregated.

When producing legal entities cuts of the ACVA charge (Advanced CVA), only the EE profiles relating to that entitity should be aggregated. This measn that the EE profiles should be preserved as the aggregation rules will vary by entity.

where

= time to maturity of the i-th tenor

= time to maturity of the i-th tenor

= current credit spread of the coutnerparty at tenor

= current credit spread of the coutnerparty at tenor

LGDmkt= = market implied loss given default of the counterparty

= Default risk-free discount factor at time horizon

= Default risk-free discount factor at time horizon

These Cs01 are used to generate VaR.

Hedges

Hedges are different from exposures and are not subject to the regulatory formula. Instead, CS01 are calculated using other internal valuation models.

Market Data Used

As described in the SFT section, exposures are combined with market data to generate CS01. In cases where a counterparty has a traded CDS, this will be used as the source of the credit spread and market-implied LGD.

Where counterparties don’rt have a traded CDS, that counterparty will be mapped to a suitable proxy. In some instances this wil be another similar counterparty (possibly with a multiplier applied to take account of the differences between the two) or a combination of counterparties, but in other cases the counterparty will be mapped to a generic rating-based curve that has been constructed from traded CDS indices.

Where a suitable mapping does not exist in the proxy mapping table, and the counterparty does not have a traded CDS, a generic rating -based mapping matching the rating, sector and currency of the counterparty. this Proxy mapping process is also applied to all counterparties.

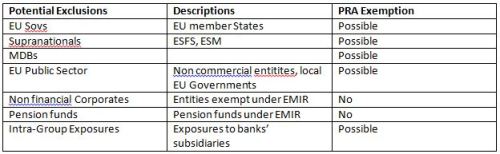

CRR Exclusions

The EU plans to consider granting exemptions for certain exposures from the CVA capital charge. The suggested exemptions are set out in a draft

Counterparties without liquid traded CDS or debt

Basel III rules mandate that counterparties without liquid market data (traded CDS or debt) shoudl be mapped to appropriate MD based on rating, sector and region.

CEM Exposure

CEM exposures are included in the CVA charge for all EU regulators. For PRA, the materiality of the CEM exposures must be assessed to determine whether they shoudl be included in the ACVA or SCVA charge.

CEM contribution= CEAM Ead/Total CEM Ead

Where:

CEM Ead is the EAD for the entity from CEM Exposures

Total EAD is the Exposure at Default for the entity from all exposures (IMM and CEM)

SFT Exposures

SFT exposures are not included in the CVA charge for PRA unless the materiality threshold is breached. The materiality of such exposures must be assessed for CVA inclusion. Threshold is calculated as follows:

SFT contribution= SFT Ead/Total EAD

Where:

SFT Ead is the EAD for the entity from SFT exposures

Total EAD is the EAD from all exposures